Report confirms middle-market doldrums

A decade of dwindling growth has hurt weakened midtier federal professional services companies.

“Structure and Dynamics of the U.S. Federal Professional Services Industrial Base”

A new think tank study confirms what many federal services executives have known for some time: the middle market is a tough place to play.

The Center for Strategic and International Studies’ report, “Structure and Dynamics of the U.S. Federal Professional Services Industrial Base,” chronicles the rise of the federal services market, from $102 billion in 1995 to $167 billion in 2004, the last year the study considered. Information and communications services were the fastest growing segment of the market, expanding at a 14 percent compound annual growth rate between 1995 and 2004.

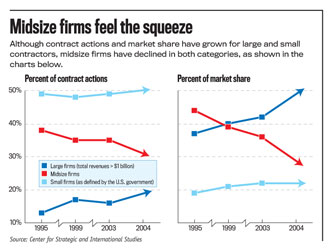

Conversely, the report also documents the dwindling market reach of middle-market services providers, which CSIS defines as being larger than government-defined small businesses and below the $1 billion revenue threshold.

According to CSIS, midtier companies commanded 44 percent of the federal services dollars in 1995, but their slice of the market had slipped to 29 percent by 2004.

During that time, the market share of large businesses grew from 37 percent to 49 percent, while small businesses stabilized in the 19 percent to 22 percent range.

“We’ve been seeing a squeeze on midtier companies for the last five years,” said Jim Kane, president and chief executive officer of the Systems and Software Consortium. Kane, who was briefed on the CSIS report, said the study quantifies the trends that many have observed.

The study raises questions that must be considered, said Stan Soloway, president of the Professional Services Council, the industry association that requested the CSIS study. Soloway said he hopes not to see an environment in which the only way to survive is to be either a giant company or a small company with a protected market. “Can we maintain balance in the marketplace?” Soloway asked.

The middle sector is the most problematic in the federal services market because midsize companies “have been squeezed from above by consolidation and from below by small businesses holding onto their share of the market,” the report states.

Pierre Chao, a senior fellow at CSIS and the report’s project director, said anecdotal evidence suggests that some small businesses “are really reluctant to leap into the middle tier and leave the protection of the set-aside world, which is an issue in terms of repopulating the middle tier.”

Once they move beyond the relative safety of set-aside contracts, middle market companies face competition from the industry’s heavyweights. They may also find potential contract opportunities embedded within large — and therefore difficult to pursue — contract vehicles. “Contract bundling is taking business away from the midtier companies,” said Lloyd Chapman, president of the American Small Business League.

To avoid the middle market, companies may seek to maintain their small-business qualifying size or choose to sell out to a larger firm, Chao said. Input released a report earlier this year that supports the latter as the more common choice. The market research firm assessed 85 deals for which the seller’s revenue was available and found that two-thirds of them had revenue of less than $50 million.

Despite the middle market’s difficulties, some companies have prospered. SI International, which earned $397.9 million in revenue last year, reported a 20 percent increase in new business, not including revenue from recently acquired companies, last year and 18 percent in 2004. “We haven’t seen any erosion,” a company spokesman said.

ITS, an IT solutions provider, graduated from the small-business category and is now a $100 million business. Rosanne Satterfield, a senior vice president at ITS who joined the company in 1998 when it was a $5 million firm, said small businesses must invest in infrastructure and develop a strategic growth plan to succeed. ITS’ plan depends on organic growth, strategic acquisitions and partnerships with large and small businesses. Satterfield said the company aims to hit the $250 million revenue mark by 2008.

Kane said midtier companies can counteract their size disadvantage by focusing on technical leadership. “Large companies take advantage of economies of scale,” he said. “But successful midtier companies are those that have been able to leverage economies of skill. There’s already room for those midtier companies.”

One CSIS finding cuts across all strata of the professional services market. The average size of a contract declined significantly during the 10-year span of the study, dropping 30 percent to $271,000 in 2004. The decrease stems from the government’s increased use of multiple-award contracts through which agencies conduct numerous task-order competitions.

That trend means that service providers “have to run harder just to stand still in the marketplace,” Chao said. “It’s a marketplace that is getting increasingly competitive.”

And more difficult to penetrate. Chao said half of the services market in any given year consists of modifications to existing contracts and large, multiple-award contracts. “That tells you the only way to grow is to either get one of these larger vehicles or do acquisitions,” he said.

Click here to enlarge chart (.pdf).

NEXT STORY: Alliant contracts move ahead